As more countries roll out e-invoicing mandates, the global business landscape is entering a new phase defined by digital integration, data-driven insight, and greater efficiency.

This shift is a chance for businesses to make their operations smoother, tighten financial control, and step up digital maturity. Organizations that approach this change proactively will not only avoid regulatory pitfalls but will also unlock significant operational advantages.

Here, we take a look at the shift towards e-invoicing, the countries that are leading the way, and why it’s important for organizations to plan ahead.

What is e-invoicing?

First, let’s clarify what we mean by mandated e-invoicing. E-invoicing refers to the structured, automated, and end-to-end electronic exchange of invoice data between a supplier’s and buyer’s financial systems, often with government insight.

This process relies on two key components:

- Structured data: Invoices are generated in machine-readable formats like XML (Extensible Markup Language) or UBL (Universal Business Language). This allows software to automatically process the data without manual intervention, eliminating keystrokes and errors.

- Interoperability networks: The Peppol network (Pan-European Public Procurement On-Line) is becoming the de facto standard. Think of it as a secure, standardised postal service for electronic documents, ensuring that any connected business can send and receive e-invoices to any other business, irrespective of the software they’re using.1

Some governments, particularly in the EU, are moving towards Continuous Transaction Controls (CTC), where invoice data is reported to or validated by tax authorities in near-real time. This is a significant step beyond post-audit reporting and is designed to create a live, digital chain of transaction truth.

The global context: A wave of digital reporting

Mandatory e-invoicing is a well-established, global trend. Latin American countries like Brazil have had mandatory e-invoicing for years. Brazil’s Nota Fiscal Eletrônica (NF-e) has been instrumental in dramatically reducing its tax gap and increasing efficiency. In Asia, India has successfully rolled out a robust GST (Goods and Services Tax) e-invoicing system for large enterprises.

In the EU, all public administrations must be able to receive invoices. In most cases, if you are a supplier in the EU, you can choose whether to send one or not. Each EU country has its own rules around e-invoicing, and it could be mandatory to send them for public contracts in some countries. You can review specific rules by country here.

In the UK, a consultation earlier this year gathered views on standardizing e-invoicing and how to increase adoption across UK businesses. The findings are due to be published soon.

The governmental drivers behind e-invoicing

Governments are pursuing this agenda for several reasons:

- Closing the VAT gap: The primary driver is combating tax fraud and evasion. The VAT gap, the difference between expected VAT revenue and the amount collected, was estimated at ~€89 billion in 2022 in the EU alone.2 In the UK, the VAT gap was estimated at ~£8.9 billion for the 2023-2024 tax year, which represents 5% of total VAT liabilities per HMRC’s (HM Revenue & Customs) 2025 edition.3 Real-time e-invoicing makes it significantly harder to hide transactions or issue fake invoices, directly addressing this revenue loss.

- Boosting efficiency: These mandates often start with public procurement. The UK government, for instance, has mandated NHS suppliers to use e-invoicing to streamline processes and reduce administrative costs for the public sector.

- Levelling the playing field: Ensuring all businesses, domestic and cross-border, comply with the same standards fosters equitable competition and reduces the administrative burden of cross-border trade within the EU.

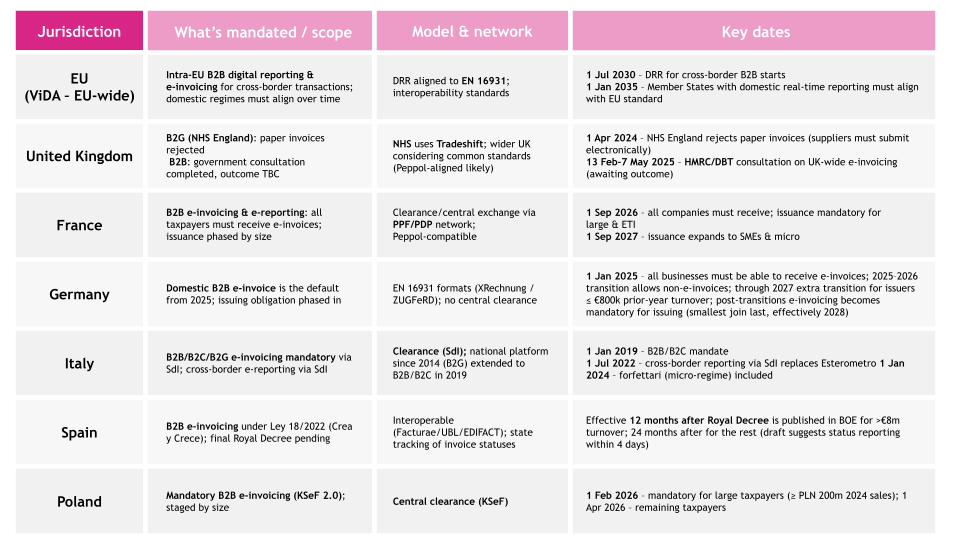

Scope and timelines: A detailed look at the UK and EU roadmaps

Understanding the phased and sometimes fragmented rollout is critical for business leaders to plan effectively. The landscape differs significantly between the EU and the UK.

The European Union: The ViDA framework and leading adopters

The EU is creating a harmonized framework through the VAT in the Digital Age (ViDA) proposal, but several member states have already implemented changes.

- The ViDA timeline: Following negotiations, the original ViDA timeline has been delayed. The current, more realistic expectation is a phased implementation:

- From 1 July 2030, intra-EU B2B transactions move to e-invoicing + Digital Reporting Requirements (DRR).

- By 1 January 2035, Member States that already run domestic real-time reporting/e-invoicing must align their systems to the EU model (it does not force every country to introduce a domestic clearance system).4

- Front-runner member states: Several EU countries have already implemented or are advancing their own domestic mandates, creating an immediate compliance burden for businesses operating there, including:

- France: 1 Sept 2026: all companies must receive e-invoices; large & ETI begin issuing (with e-reporting). 1 Sept 2027: SMEs/micro begin issuing.5

- Germany: 1 Jan 2025 all businesses must be able to receive EN 16931 e-invoices. Issuing becomes mandatory 1 Jan 2027 for businesses with >€800k turnover; 1 Jan 2028 for all others.6

- Poland: The KSeF (National E-Invoicing System) KSeF mandatory 1 Feb 2026 for large taxpayers; 1 Apr 2026 for all others.

- Romania: RO e-Factura B2B mandatory; invoices must be sent via the national platform within 5 days as of 1 Jul 2024.

- Spain: SII is near-real-time VAT ledger reporting, not B2B e-invoicing. Spain’s B2B e-invoicing under ‘Crea y Crece’ starts 12 months after the Royal Decree for large companies, 24 months for others, earliest 2026/2027, pending the decree.7

- Italy: The tax authority’s Sdl (Sistema di Interscambio) clearance platform mandates e-invoicing–B2B/B2C since 2019 (B2G since 2014/15)--with invoices transmitted in FatturaPA (XML).

The UK: A phased and cautious approach

The UK is taking a more gradual, sector-led approach compared to the EU’s broader proposal.8

Live mandate - B2G (Business-to-Government)

- NHS England: As of April 2024, all suppliers contracting with NHS England are required to use the NHS P2P system for e-invoicing. This is a de facto mandate for a significant portion of the UK’s public sector supply chain.9

- Wider public sector: While not a single, unified law, many central government departments already require Peppol-based e-invoicing for suppliers, a practice that is steadily expanding.

Proposed mandate - B2B (Business-to-Business)

- The catalyst: The Spring 2024 HMRC consultation “Making Tax Digital for Business: The Future of Tax Administration” is the key document. It explicitly explores the introduction of a B2B e-invoicing and digital reporting mandate.

- Timeline: Based on the consultation timeline and the need for a lengthy implementation period, a widespread B2B mandate is not expected before April 2026, and more likely April 2027 or later.

- Key UK differentiator: The UK model is expected to be a “Clearance Model,” where invoices are reported to HMRC after issuance (periodic digital reporting), rather than the real-time pre-clearance model used in some countries, such as Italy or Spain. This critical design detail will affect system requirements.

The operational impact of e-invoicing across departments

The impact of this shift will be felt far beyond the finance department.

- Finance & AP/AR transformation: Manual processing will decline, leading to lower costs and fewer errors. This can drastically reduce invoice approval cycle times, unlocking opportunities for improved payment terms and dynamic discounting, thereby optimizing working capital.

- Supplier & partner management: The biggest challenge may be onboarding your entire supply chain. Educating and technically enabling smaller suppliers who lack digital sophistication will be critical. This becomes a point of strategic relationship management, which can be either a collaboration opportunity or a significant source of friction.

- Technology & systems: Your current ERP and Procure-to-Pay (P2P) systems (e.g., SAP, Oracle, Coupa) will likely require configuration, upgrades, or new middleware to connect to networks like Peppol. Integration intricacy between your e-invoicing platform, ERP, and other financial systems cannot be underestimated.

Compliance as an opportunity

Adopting a minimal-compliance, “checkbox” mentality would be a missed opportunity. Forward-thinking organizations will leverage this change to:

- Optimize working capital: Faster invoice approval cycles improve cash flow forecasting and unlock early payment discounts.

- Harness data-driven insights: Rich structured data from e-invoices is a goldmine for metrics, including spend analytics, enabling smarter strategic sourcing and supplier negotiations.

- Strengthen supply chain resilience: Proactively helping suppliers to adapt will build loyalty and strengthen the entire value chain

- Accelerate digital transformation: This is the catalyst to modernize legacy P2P processes holistically, embedding automation and intelligence at the core of your financial operations.

The move to mandatory e-invoicing is imminent and will be transformative. By starting your planning now and viewing this mandate through a strategic lens rather than just a compliance one, you can position your organization to emerge more efficient, agile, and data-driven. The future of finance is digital, interconnected, and transparent.

Planning your move to e-invoicing?

You don't have to navigate the complexities of ViDA, Peppol, and ERP integration alone. Whether you're just starting your plan or are deep in supplier onboarding, our experts can provide the clarity you need.

Get in touch to find out how we guide organizations through the entire e-invoicing journey, from initial strategy to full-scale implementation.

Disclaimer:

This article is provided for general information purposes only and does not constitute legal advice. The content in this article is not a substitute for professional advice. You should seek independent legal advice to obtain a full analysis of the relevant legislation and its application to your particular circumstances.

This article is based on current regulatory announcements, including the EU's ViDA implementation strategy, national government publications, and global industry analysis as of October 2025. Regulations continue to evolve; strategic advice should be tailored to your organization’s specific context and jurisdictions of operation.

Footnotes

1. openpeppol.atlassian.net/wiki/spaces/VP/overview

2. https://data.europa.eu/doi/10.2778/2476549

3. https://www.gov.uk/government/statistics/measuring-tax-gaps/1-tax-gaps-summary

4. taxation-customs.ec.europa.eu/news/adoption-vat-digital-age-package-2025-03-11_en

5. www.bdo.global/en-gb/insights/tax/indirect-tax/france-mandatory-e-invoicing-to-be-implemented-in-2026-updates-on-preparations

6. e-rechnung-bund.de/en/faq/

7. sede.agenciatributaria.gob.es/Sede/en_gb/iva/regimenes-tributacion-iva.html

8. www.gov.uk/government/publications/procurement-act-2023-guidance-documents-manage-phase/guidance-electronic-invoicing-and-payment-html

9. www.sbs.nhs.uk/services/finance-and-accounting/p2p-purchase-to-pay/